On today’s market, every savvy seller wants to know what turns buyers off, so they can get their homes sold as quickly as possible, for as much as possible. But buyers, take note – there is a minefield of seller turn-offs you can trigger that hold the potential to keep you from getting the home you want at the best price and terms, or to unnecessarily complicate dealings with your home’s seller.

Lest you think all of today’s sellers are under the gun and will just put up with whatever behavior buyers dish out, be aware that there are still many multiple offer situations in which buyers have to compete with each other to get a home – buyers who trigger these turnoffs tend to lose in those scenarios. Also, avoiding these seller turnoffs can create a transactional environment of cooperation and avoid things turning adversarial. That, in turn, can empower you to score a better price, get extra items you want thrown into the deal, and even negotiate more flexibility around your escrow and move-in timelines – all perks that can make your life easier and your budget go further.

For sellers, these turnoffs pose the potential of irritating you out of an otherwise good deal – maybe even the only deal you have!

Here’s a few of the most common buyer-perpetuated seller turnoffs, with tips for sellers on how to keep an emotional (and economic) even keel, even if your home’s buyer makes some of these waves:

1. Trash-talking. Trash-talkers are the home buyers who think they’re going to negotiate the list price down by slamming the house, telling the sellers how little it is really worth, how the house across the street sold for nothing, why the school on the corner should make them desperate to give the place away, etc. This strategy never works; in fact, when you attack a seller and their home, you only cause them to be defensive, and think up all the reasons that (a) their home is not what you say it is, and (b) they shouldn’t sell their home to you!

Sometimes this happens with buyers who actually love a house and just walk around it fantasizing about all the ways they would customize it to their tastes while a seller is there. Sellers: avoid being at home while your home is being shown. Buyers: save your commentary for your agent; if you do encounter the seller in person keep your conversation respectful and avoid critiquing the house or the list price.

2. Being unqualified for mortgage financing. When a seller signs a buyer’s offer, most often the seller agrees to effectively pull the home off the market, forgoing other buyers who might be interested. As such, the only thing worse than getting no offers on your home is getting an offer, getting into contract, then having the whole thing fall apart when the buyer’s loan falls through – especially if that could have been predicted or avoided up front.

Sellers: Work with your agent to vet your home’s buyers’ qualifications, including their loan approval, down payment and earnest money deposit – before you sign a contract. It’s not overkill for your agent to call the buyers’ mortgage pro before you sign the contract and get a level of comfort for how robust their qualifications are. Buyers: Get pre-approved. Seriously. And make sure that you don’t buy a car, quit your job, deposit lottery winnings or do any other financial twitchery between the time you get loan approval and the time you close escrow on your home.

3. Making unjustified lowball offers. No one likes to feel like they are being taken advantage of. And sellers generally know the ballpark amount that their home is worth, as well as what they need to sell it for to get their mortgage paid off. Yes – the price you pay for a home should be driven by its fair market value, rather than the seller’s financial needs, and deals are more available in a market like the current one, in which supply so vastly outpaces demand. But just throwing uber-lowball offers out at sellers hoping one will hit the spot is not generally a successful strategy, especially if you really, really want a given property.

Sellers: Don’t get overly emotional about receiving a lowball offer; counter at the price you and your agent decide makes sense based on the total circumstances, including your motivation level, recent comps and the interest/activity level your listing is receiving. Buyers: Work through the similar, nearby homes that have recently sold (a/k/a comparables) before you make an offer to factor the home’s fair market value into your offer price – also factor in how much you want the place, too. Don’t be amazed if you make an offer far below asking, and don’t get a response.

4. Renegotiating mid-stream. Sellers plan their finances, moves and - to some extent – their lives around the purchase price a buyer agrees to pay for their home. If you get into contract to buy a home, find out during inspections that costly repairs need to be made, then propose a lower sale price, repair credit or even actual repairs to the seller, that’s sensible and fair. But if you were aware that the property needed a lot of work before you made an offer on it, then you come back asking for beaucoup bucks’ worth of credit or price reductions midstream, expect the seller to cry foul. And holding the seller up two weeks into the transaction because you caught a case of buyer's remorse? Not cool, and not likely to foster the spirit of cooperation you may need to get your deal closed.

Sellers: avoid mid-stream price renegotiations by having a full set of inspection reports and repair bids at hand when you list your home. Buyers: try to avoid renegotiating the entire deal unless you get some major surprises at your inspections or inflating small repairs to try to justify a major price cut.

5. Misleading or setting the seller up. Remember when we talked about buyer turn-offs? Being misled by listing photos or very fluffy property descriptions was high on the list. The same goes for sellers.Offering way over asking with the plan to hammer the seller for a reduction when the house doesn’t appraise at the purchase price? #LAME Making an as-is offer planning the whole time to come back and ask for every penny ante repair called out by the inspectors? Lame squared.

Sellers: If you get multiple offers and are tempted to take a sky-high one or one that claims to be all cash, consider requesting proof that the buyer has sufficient funds to make up the difference between what you think the home will appraise for and the actual sale price, and statements showing the cash truly exists. Buyers: Don’t be lame. I’m not saying you have to tell the seller exactly what your top dollar is, but making offers with terms designed to intentionally mislead is really, really bad form – and can result in losing the home entirely if and when your bluff gets called.

Tuesday, April 12, 2011

Friday, April 8, 2011

Unemployed Loan Program Now Available!!!

It's here! Unemployed homeowners can now receive loans that will help them avoid foreclosure, thanks to a new program by the Obama administration.

After delays and efforts to terminate the program, the $1 billion Emergency Homeowners' Loan Program–established when the Dodd-Frank financial overhaul bill was enacted in the summer of 2010–is now ready to help unemployed homeowners to continue to make their mortgage payments.

The program will allow qualified unemployed homeowners to receive zero-interest loans of up to $50,000 and for up to two years. The loan can be forgiven if the homeowner stay in the house five years. Requirements include being at least three months behind on your payments but also having a reasonable ability to resume payments within the two-year period. Additionally, homeowners have to have had a 15% decrease in income. However, they must have been able to pay for their mortgage prior to the income drop. They can't own a second home and the property has to be their primary residence.

Included in this latest emergency relief effort are: Pennsylvania ($106 million), Maryland ($40 million), Connecticut ($33 million), Idaho ($13 million), and Delaware ($6 million).

Coming soon, nonprofit NeighborWorks America, is providing federal funding for loans in 27 other states that don't have a similar program. The Department of Housing and Urban Development expects some 30,000 homeowners to participate.

Other states such as California, Nevada, Michigan, and a few more are expecting to receive some aid through the Treasury Department, which has allotted $7.6 billion in assistance for hard-hit states.

Meanwhile, housing-market analysts are saying that for long-term real estate recovery to occur, live-in homebuyers are necessary. Experts acknowledge that markets such as Phoenix, Arizona were propped up by very low interest rates, investor demand, and some of the most affordable home prices ever seen.

But experts say that buyers who are purchasing to live in the home will help stimulate the housing recovery process. In some markets, like Phoenix, it's been a 50-50 split between live-ins and investors.

Some of the factors holding back traditional buyers from dominating the market are, of course, stricter requirements for lending, unemployment, or lack of sufficient work, and uncertain financial times.

Live-in homebuyers tend to come from one of two groups: first-time or move-up buyers. With the recent marketplace and economic conditions being so unstable, and a decline in home value, the move-up buyers have not been very active. But some real estate experts are seeing an emergence of a new buyer group: lower-income residents. This group can now afford to buy because the home prices, in some areas, have declined significantly. However, in many areas, home investors are vying for those same properties, creating competition.

In a perhaps surprising move, some home auctions, where investors can typically scoop up a great deal, are now excluding investors. A California-based firm is helping to get rid of all foreclosed Arizona homes for which the previous owners had U.S. Federal Housing Administration-backed loans. The U.S. Department of Housing and Urban Development's policy gives traditional buyers at least 30 days to bid on new listings first. Then the properties may be opened up to investors. Homes in the Phoenix area are being sold online at HudHomeStore.com.

After delays and efforts to terminate the program, the $1 billion Emergency Homeowners' Loan Program–established when the Dodd-Frank financial overhaul bill was enacted in the summer of 2010–is now ready to help unemployed homeowners to continue to make their mortgage payments.

The program will allow qualified unemployed homeowners to receive zero-interest loans of up to $50,000 and for up to two years. The loan can be forgiven if the homeowner stay in the house five years. Requirements include being at least three months behind on your payments but also having a reasonable ability to resume payments within the two-year period. Additionally, homeowners have to have had a 15% decrease in income. However, they must have been able to pay for their mortgage prior to the income drop. They can't own a second home and the property has to be their primary residence.

Included in this latest emergency relief effort are: Pennsylvania ($106 million), Maryland ($40 million), Connecticut ($33 million), Idaho ($13 million), and Delaware ($6 million).

Coming soon, nonprofit NeighborWorks America, is providing federal funding for loans in 27 other states that don't have a similar program. The Department of Housing and Urban Development expects some 30,000 homeowners to participate.

Other states such as California, Nevada, Michigan, and a few more are expecting to receive some aid through the Treasury Department, which has allotted $7.6 billion in assistance for hard-hit states.

Meanwhile, housing-market analysts are saying that for long-term real estate recovery to occur, live-in homebuyers are necessary. Experts acknowledge that markets such as Phoenix, Arizona were propped up by very low interest rates, investor demand, and some of the most affordable home prices ever seen.

But experts say that buyers who are purchasing to live in the home will help stimulate the housing recovery process. In some markets, like Phoenix, it's been a 50-50 split between live-ins and investors.

Some of the factors holding back traditional buyers from dominating the market are, of course, stricter requirements for lending, unemployment, or lack of sufficient work, and uncertain financial times.

Live-in homebuyers tend to come from one of two groups: first-time or move-up buyers. With the recent marketplace and economic conditions being so unstable, and a decline in home value, the move-up buyers have not been very active. But some real estate experts are seeing an emergence of a new buyer group: lower-income residents. This group can now afford to buy because the home prices, in some areas, have declined significantly. However, in many areas, home investors are vying for those same properties, creating competition.

In a perhaps surprising move, some home auctions, where investors can typically scoop up a great deal, are now excluding investors. A California-based firm is helping to get rid of all foreclosed Arizona homes for which the previous owners had U.S. Federal Housing Administration-backed loans. The U.S. Department of Housing and Urban Development's policy gives traditional buyers at least 30 days to bid on new listings first. Then the properties may be opened up to investors. Homes in the Phoenix area are being sold online at HudHomeStore.com.

Wednesday, April 6, 2011

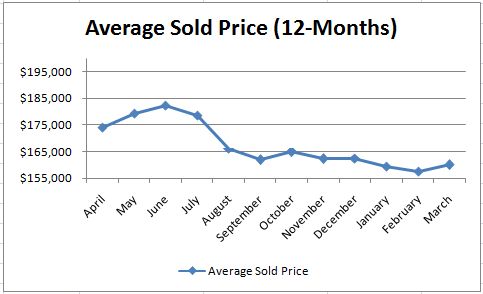

PHOENIX REAL ESTATE MARKET REPORT - MARCH 2011

Phoenix Real Estate Market Report Summary

This data includes single family detached homes, patio homes, condos, and townhomes provided by the Arizona Multiple Listing Service. The monthly charts above are based on trailing twelve monthly averages from April 2010 to March 2011 which shows the total activity in the Phoenix Metropolitan real estate market over a twelve month period. The yearly charts above are based on a yearly average for 2005 to 2009 but a trailing twelve month average from April 2010 to March 2011 for the year 2011. Without the trailing twelve month average for the year 2011, the charts would be substantially skewed and would not portray an accurate view of the market on an annual basis.

Since the expiration of the first time home buyer tax credit on April 30, 2010, the real estate market has decreased in the average sold price and number of transactions. Since April 2010, the average sold price has decreased approximately -8.1% (up from last month), the average days on market have increased approximately +17.7% (down from last month) and the number of transaction has increased approximately 8.2% (up substantially from last month). Since April 2010, the number of sold bank owned foreclosures has increased approximately 15.7% (doubled since last month) and the number of short sale has increased only approximately 4% (up slightly from last month). Based on this information, it appears there is an oversupply of properties on the market and if banks continue to add more foreclosure inventory to the market, then this will continuing to cause prices to fall. It also appears demand in the market is stronger than the prior year and the results can be seen in the increased number of transactions. If demand for real estate exceeds supply, then price will start to appreciate once again. The peak buying season in the Phoenix market generally does not begin until March or April and then slows down slightly in July and August.

The number of Notice of Trustee Sales is currently experiencing a decline due to increased government intervention to make lending institution work hard on helping people stay in their homes. The number of foreclosures “notices” entering the market is expected to decline in late 2011 and early 2012 due to the exhaustion of adjustable rate mortgages created between 2003 to 2007. Although the number of foreclosure notices will decline, there are still a lot of homeowners upside down and a lot of these homeowners will make a business decision to let their homes go into foreclosure despite the fact they can continue paying their mortgage. The number of trustee’s deeds issued at the trustee auctions is on a steep incline which means the competition for trustee properties has increased over the last two months due to the lower supply of foreclosure. There is a large amount of properties sold at the court house steps but there is still a large amount of REO properties sold through the MLS. According to the above market statistics, the demand for trustee sale foreclosures has increase substantially and the demand for REO properties is increasing. It is impossible for real estate prices to go down much further since the market will eventually reach a level of equilibrium where demand will exceed supply and all buyers will rush into the market to take advantage of low prices before the prices start to increase. A lot of investors and home buyer have already realized that now is the best time to buyer while prices are low.

Subscribe to:

Posts (Atom)